Superbonus 110 Percent: An interesting Opportunity

The Italian Government has launched a 110 percent tax break. The “Relaunch Decree” increased the rate for the deduction of expenses for energy measures such as building insulation, earthquake protection or the installation of photovoltaic systems. These measures are known as “Superbonus 110%” and apply to work that has been carried out since 1 July 2020 or which was completed by 31 December 2021.

The tax relief consists of deductions from the gross tax and is granted when the measures carried out increase the energy efficiency or reduce the seismic risk of existing buildings.

In particular, it is available for expenses incurred for measures on common parts of buildings, on real estate units functionally independent and with one or more independent accesses from the outside located inside multi-family buildings, as well as on single real estate units.

We would be happy to discuss the rules of the ‘Superbonus 110%’ with you and support you in drafting contracts and fulfilling your obligations related to tax relief.Antonio Argenio, Partner, Tax Consultant, Certified Public Accountant, Milan, Italy

Which Measures Qualify for the Superbonus?

In detail, the highest deductions are recognised for documented expenses incurred by the taxpayer for the following measures (so-called “driving interventions”):

- Thermal insulation

- Replacement of existing winter air conditioning systems with centralised systems

- Earthquake-resistant interventions

The Superbonus is also available for the following additional measures (so-called “driven interventions”), provided that they are performed in conjunction with at least one of the previously listed driving interventions:

- Energy efficiency requalification

- Installation of infrastructure for recharging electric vehicles

The Superbonus is not available for works carried out on residential property units in cadastral categories A1 (mansions), A8 (villas) and A9 (castles), explain the Ecovis advisers.

These options are available to take advantage of the Superbonus 110% tax relief:

Who Will Benefit from the Tax Break?

- Condominiums

- Individuals, other than for properties used to carry on a business or profession

- Housing cooperatives

- Non-profit, social promotion and voluntary organisations

- Amateur sports associations and clubs

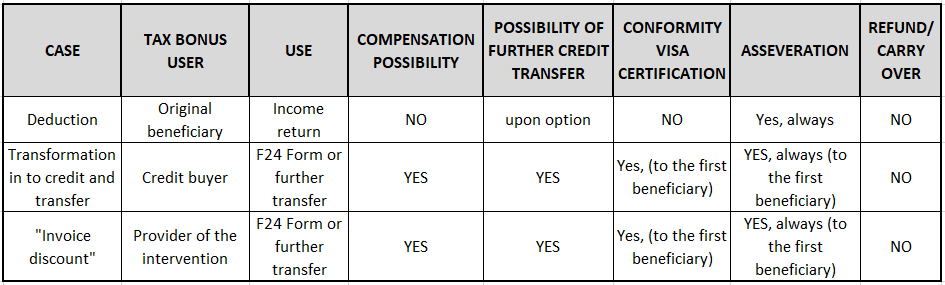

Taxpayers can decide to either keep the bonus for the purposes of tax deduction, transfer the credit, or exercise the option to request “invoice discount” through the transfer of the credit to the supplier who will carry out the works (s. info box).

In order to choose the most favourable option, it is advisable to carry out a preliminary check for the presence of income which would allow the deduction, as in the conversion phase of the Decree, the possibility of transforming the deduction into a tax credit for direct use was eliminated.

If the taxpayer decides to transfer the credit due or opt for a contribution in the form of a discount on the amount due, this must be submitted as a specific request to the Revenue Agency. The transfer can be arranged in favour of the suppliers that have carried out the works, other subjects (private persons, enterprises, companies and bodies), or credit institutions and financial intermediaries.

In addition to the regular requirements for the above-mentioned deductions, the option for transfer or discount also requires a “Conformity Visa”, which contains the technical data relating to the documentation certifying the existence of the assumptions that entitle to the tax deduction.

In all cases, the works must also be certified by a qualified professional energy efficiency or anti-seismic technician, say the advisers from ECOVIS STLex.

For further information please contact:

Antonio Argenio, Partner, Tax Consultant, Certified Public Accountant, Milan, Italy

Email: antonio.argenio@ecovis.it

Luciana Perini, Turin, Italy

Email: Luciana.perini@ecovis.it

Federica Cucut, Genoa, Italy

Email: federica.cucut@ecovis.it